Totaled Your Tesla? Here’s What Happens to Your $10,000 FSD Package

Imagine the nightmare scenario: you are involved in an accident, and your beloved Tesla is declared a total loss. Beyond the stress of the accident itself, a financial panic sets in. What happens to that $8,000, $10,000, or even $15,000 you spent on the Full Self-Driving (FSD) capability? Do you simply lose that investment?

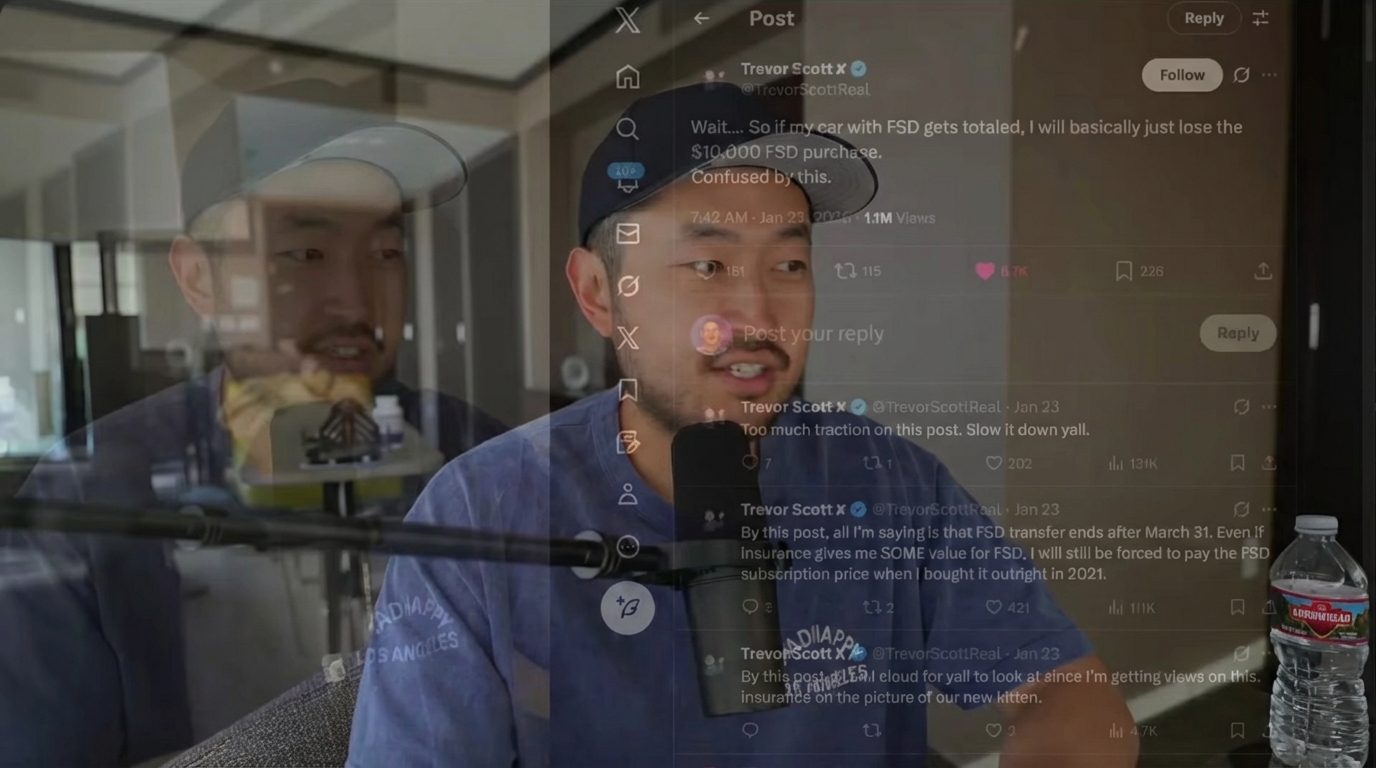

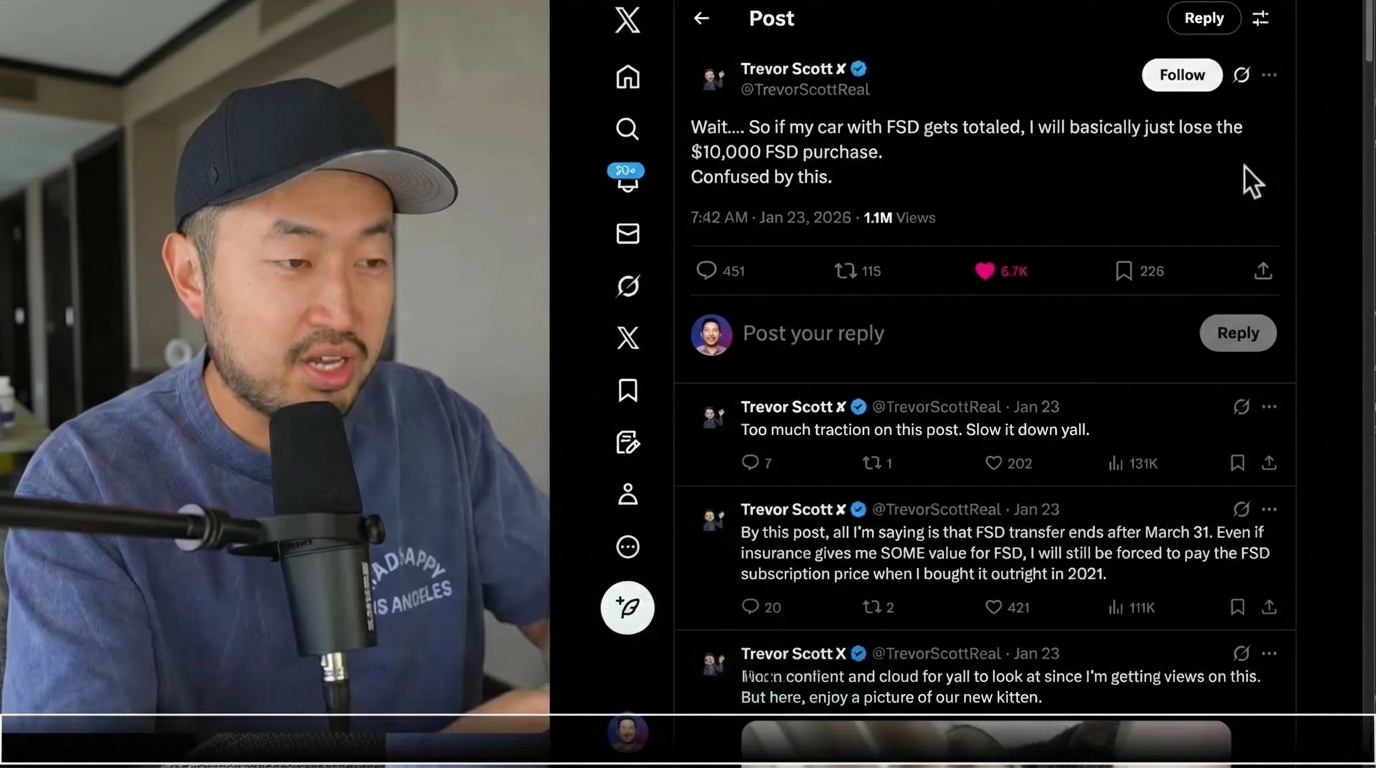

A recent viral post on X (formerly Twitter) by Trevor Scott highlighted this exact confusion. He asked, "Wait... So if my car with FSD gets totaled, I will basically just lose the $10,000 FSD purchase. Confused by this."

The short answer is: it depends. However, it is rarely a total loss if you know how to navigate the claims process. Insurance payouts are essentially negotiations, and recovering the value of your software depends heavily on how and when you bought it. Here is a breakdown of the three main scenarios and how to handle them.

1. The Factory-Installed Scenario (The Easiest Path)

If you purchased your Tesla with FSD selected at the time of ordering, you are in the strongest position. In this case, the software package is listed directly on the window sticker (the Monroney label).

Because it is part of the original factory equipment and included in the Manufacturer's Suggested Retail Price (MSRP), insurance adjusters generally factor this into the vehicle's total value automatically. It is treated no differently than upgrading to larger wheels or a premium interior.

2. The Subscription Model (The Loss)

This is the most straightforward scenario, though perhaps the least satisfying if you were hoping for a payout. If you are paying for FSD on a monthly subscription basis ($99 or $199/month), you generally hold no equity in the software. When the car is totaled, you simply stop paying the subscription. You won't get a payout for previous months' rent, just as you wouldn't get money back for gas you already used.

3. The Aftermarket Upgrade (The Negotiation)

Things get tricky if you bought the car first and then purchased FSD later through the Tesla app for a lump sum (e.g., $10,000). In the eyes of an insurance company, this is often considered an "accessory" or an aftermarket addition.

To ensure you get paid out for this, you must:

- Keep your receipts: You need proof of the purchase date and amount.

- Provide documentation: Show the adjuster that this specific vehicle has the software active.

- Negotiate: The initial offer might not include the software value. You will have to push back.

How to Win the Negotiation

Regardless of when you bought it, insurance companies often lead with a lowball offer. If the adjuster claims FSD adds zero value to the used car price, the burden of proof is on you.

The best strategy is to find comparable vehicles (comps) in the current used market. Find listings for Teslas that are identical to yours—same year, similar mileage, same trim—where one has FSD and the other does not. If the market shows that FSD-equipped cars are selling for $5,000 to $8,000 more, you can present this data to the adjuster to justify your demand for a higher payout.

Remember, an insurance settlement is a negotiation. Never accept the first check if it doesn't cover the true replacement cost of your vehicle, software included.